08 Apr

Every January, Nigerians make bold financial promises. By March, most of those promises are quietly buried under rent, school fees, fuel costs, and family obligations. The problem is never motivation. It is the planning unit.

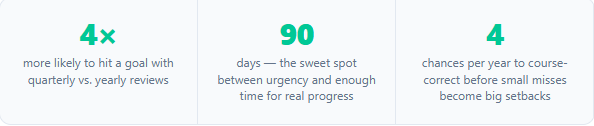

A year is too long. Your brain treats a 12-month goal as a future problem something to deal with after the next salary, the next contract, the next “right time.” But 90 days? That is real. That is now. That is where financial change actually happens.

This guide is Savey’s practical framework for the rest of 2026 built specifically for Nigerian couples, young professionals, students, and business owners who want to stop wondering where their money went and start building something that lasts.

Step 1: Run a Brutally Honest Financial Audit (90 Minutes)

You cannot plan your way forward from a number you are guessing at. Before setting any goal, spend 90 minutes with your actual bank statements. No estimates. No feelings. Just truth.

Here is exactly what to look at:

- Your real monthly take-homeEvery income stream that actually hits your account (salary, freelance, business revenue, rent income). Use what lands, not what is on your offer letter.

- Every naira that left youPull three months of bank and mobile money statements. Categorize honestly: food, transport, airtime/data, rent, school fees, subscriptions, transfers to family, entertainment. Most people are surprised usually not pleasantly.

- Your net worth right nowadd up everything you own (savings, investments, assets) and subtract everything you owe (loans, credit, owe-and-pay). Write the number down. This is your baseline. Your job is to grow it every quarter.

- Your savings rateMonthly savings ÷ monthly income × 100. If you are saving ₦20,000 from a ₦200,000 salary, that is 10%. Savey’s recommended minimum for meaningful wealth-building is 20%. This single number tells you more about your financial trajectory than anything else.

- Your top 3 money leaksWhere is money leaving with the least value in return? Common culprits in Nigeria: POS charges on small withdrawals, overlapping streaming and app subscriptions, and food delivery spending that crept up quietly.

Savey Tip

Many Nigerians are paying for 3–5 subscriptions (Netflix, Spotify, Amazon Prime, cloud storage, news apps) simultaneously often on multiple accounts. A quick audit of your debit alerts for the past month often frees up ₦5,000–₦15,000 immediately that can be redirected to a goal.

Step 2: Set Goals That Actually Hold

Vague goals produce vague results. “Save more” is not a goal. “Spend less on unnecessary things” is not a goal. A real financial goal has five qualities and without all five, it is a wish wearing a goal’s outfit.

- Specific

“Save ₦150,000 in my Savey emergency fund by June 30” not “save more.” The brain responds to specificity. Give every goal a naira amount and a calendar date. - Measurable

If you cannot check your progress weekly against a clear number, the goal cannot hold you accountable. Attach figures to everything. - AchievableStretch goals outperform comfortable ones, but impossible goals quietly destroy motivation. ₦150,000 in 90 days on a ₦120,000 salary is not a plan; it is a setup for discouragement. Be honest about what is genuinely reachable.

- RelevantConnect every goal to something you actually care about. “Build this fund so I stop borrowing at month-end” is a stronger motivator than any spreadsheet formula.

- Time-boundAssign every goal to a specific quarter with a hard end date. “By September 30, 2026” creates accountability that “eventually” will never produce.

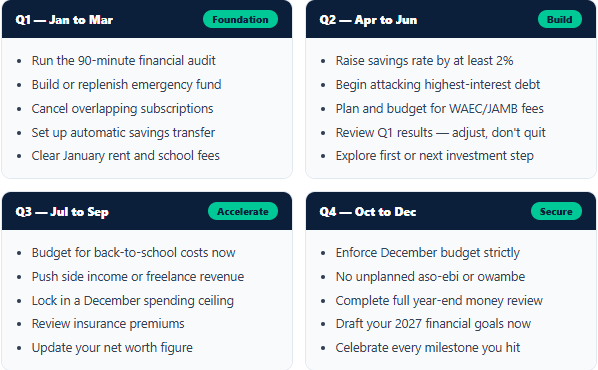

Step 3: The 2026 Nigerian Quarter-by-Quarter Playbook

Each quarter carries its own financial pressure in Nigeria. A plan that does not account for WAEC fees, Sallah spending, back-to-school costs, and December aso-ebi will be ambushed by them. This is your seasonal roadmap:

Step 4: Pick the Budget Method That Fits You Well.

The right budget is the one you will maintain past week two. Here are three proven methods, pick the one that matches how you actually think and live:

50/30/20 For beginners and anyone who has never budgeted consistently

Split your take-home income: 50% to needs (rent, food, transport, school fees, utilities, minimum loan payments), 30% to wants (eating out, entertainment, data beyond work use), and 20% to savings and debt repayment.

On a ₦200,000 take-home: ₦100,000 for needs, ₦60,000 for living, ₦40,000 building your future. Simple enough to start tonight.

🇳🇬 Nigeria Reality Check

In Lagos, Abuja, and Port Harcourt, rent alone can consume 40–50% of take-home for many earners. If the 50% needs bucket is not realistic for your situation, start with 65/15/20 — keeping the 20% savings rate non-negotiable and adjusting the wants and needs split as your income grows.

Zero-Based Budgeting, For goal-driven, detail-oriented people

Every naira gets a job before the month begins. Income minus all allocations equals zero. Not because you spend everything but because every naira is intentionally directed. This method works especially well for business owners and freelancers with variable monthly income.

Pay Yourself First, For anyone who struggles with consistency

The moment your salary or revenue hits, transfer your savings amount out immediately before bills, before groceries, before anything. Then live on what remains. This eliminates the “I will save whatever is left” trap, which for most people means saving nothing. Savey’s auto-save feature is built exactly for this method.

Step 5: Build Your Emergency Fund Before Anything Else

The emergency fund is not optional, and it is not a savings goal like any other. It is the financial shock absorber that makes every other goal possible. Without it, one medical bill, one car breakdown, or one month of reduced income forces debt often at brutal interest rates from lenders, cooperative societies, or family.

Keep your emergency fund in a separate, interest-earning account accessible within 24 hours but not so accessible you will dip into it for non-emergencies. Never invest this money in anything subject to market risk.

Step 6: Attack Debt in the Right Order

Not all debt is equal. High-interest debt particularly loans from digital lenders, buy-now-pay-later services, and some cooperative society loans can charge anywhere from 3% to 30% per month in Nigeria. No investment offers a guaranteed return that beats paying off debt at those rates. Eliminating it is the highest-certainty financial move available.

Debt Avalanche (saves the most money): List all debts highest interest rate first. Pay minimums on all, direct every surplus naira at the highest-rate debt. Once cleared, roll that full payment onto the next. Mathematically optimal.

Debt Snowball (easiest to sustain): List debts smallest balance first. Clear the smallest one first regardless of rate. The psychological momentum of fully eliminating one debt keeps many people going when avalanche calculations alone would not. Choose this if you need visible wins to stay motivated.

Step 7: Start Investing, Even on a Small Income

The most expensive investing mistake is waiting. Every quarter you delay costs more than the previous quarter not just the return on the money you did not invest, but the return on every future return it would have generated. This is compounding, and it does not care about your income level. It rewards consistency.

A practical Nigerian investment priority order for 2026:

- Emergency fund first (always)No investment vehicle is worth touching before this foundation exists. Full stop.

- Treasury Bills via the CBN or your bankLow risk, naira-denominated, backed by the federal government. Current rates have been attractive in 2026 check with your bank for the latest figures. A solid starting point for first-time investors.

- Money market or mutual fundsPooled, managed funds accessible through licensed fund managers and several Nigerian fintech platforms. Liquid, regulated, and historically more competitive than standard savings account rates.

- Dollar-denominated savingsGiven naira depreciation trends, holding a portion of savings in USD through a licensed domiciliary account or regulated platform helps protect purchasing power. Start small even 5–10% of savings as a hedge is meaningful.

- Equities on the NGXLong-term investing in Nigerian Stock Exchange-listed companies. Higher risk, higher potential return. Only appropriate once emergency fund and shorter-term goals are secured. Start with a small, regular contribution rather than a lump sum.

One Rule That Always Applies

Only invest money you will not need for at least 12 months. Short-term money belongs in savings. Long-term money belongs in investments. Mixing the two forces you to sell at the worst possible time.

Step 8: Build the Review Habit That Keeps Everything on Track

People who review their finances regularly outperform those who do not regardless of income level or starting position. The review habit is the single highest-leverage financial behaviour you can build this quarter.

The Weekly 10-Minute Check-In. Every Sunday.

Three questions:

How much did I spend vs. plan this week?

Am I on pace for my quarterly goal?

What one thing do I adjust next week?

Ten minutes. Every week. People who do this almost always hit their quarterly targets.

The Quarterly 60-Minute Review. End of every quarter. Did I hit the goal? What drove overspending? What is the single priority for next quarter? What is my updated net worth? This is where course correction happens — before a difficult quarter becomes a difficult year.

✅ 5 Questions for Every Quarterly Review

1. Did I hit my savings or debt target?

2. Which spending categories overran budget, and why?

3. What single habit had the most positive impact?

4. What unexpected expense hit, and how do I plan for it next quarter?

5. What is my one priority focus for the next 90 days?

Five Mistakes That Will Quietly Derail 2026

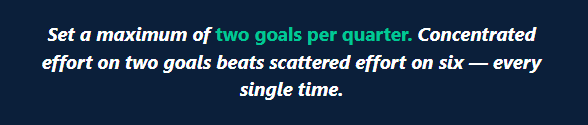

Setting too many goals at once

Two goals per quarter, maximum. Financial attention is finite. Spreading it across five goals guarantees shallow progress on all of them and full achievement on none.

Relying on willpower instead of automation

Manual savings transfers require you to make the right decision every single month. Automation makes the right decision for you, every time, without fail. Set up a standing order. Let the system do the work.

Spending every raise before saving it

The moment income increases, commit to saving at least 50% of the increment before adjusting lifestyle. This one habit, consistently applied, separates people who build wealth from those who simply earn more and spend more.

Investing before building an emergency fund

This sequence destroys more financial plans than any other. When the emergency arrives and it will you are forced to liquidate investments, often at a loss, and often at the worst possible time.

Treating a bad month as a failed plan

One overspent month is data, not defeat. Adjust the next month’s plan, understand what happened, and continue. Financial resilience, the ability to keep going after a setback predicts long-term success more reliably than any other trait.

Your 30-Day Action Plan (Start This Week)

- Week 1: The honest auditPull three months of bank and mobile money statements. Calculate real income, real expenses, real net worth. Find your top three spending leaks. No judgment just accurate data.

- Week 2: Two SMART goals on paperWrite them down with specific naira amounts, hard deadlines, and one sentence explaining why each one matters to you personally. Pin them somewhere visible.

- Week 3: Build the infrastructureChoose your budget method. Set up an automatic savings transfer for your next payday. Open a separate account for your emergency fund if you do not have one. Configure Savey to track your categories.

- Week 4: Activate accountabilitySchedule your first Sunday check-in. Set a calendar reminder for your September 30 quarterly review. Make the first automatic transfer happen. You are now running the system not just planning to.

Start Budgeting with Savey Today

Set goals, automate savings, and track every naira built for how Nigerians actually manage money.

The gap between where most Nigerians are financially and where they want to be is not an income gap. It is an execution gap. The information exists. The tools exist. What most people are missing is a structure that makes consistent execution possible even when life is expensive, unpredictable, and relentless.

The quarterly framework is that structure. Not perfection. Not a shortcut. Just a reliable system that gives you four chances every year to build, correct, and compound your progress.

The next 90 days begin today.

Download the Savey app or subscribe to join the conversation and leave a comment.